P11d forms reporting benefits in kind provided to employees and directors need to be submitted to HMRC by 6 July. Where a company car is “unavailable” for private use for 30 or more consecutive days the benefit is proportionately reduced.

During the various lockdown periods many employees and directors have not been using their company cars and it may have been sitting on their driveway. Unfortunately, that does not count as being unavailable.

HMRC have confirmed that they would continue to regard the car as available to the employee unless the keys or fobs are returned to the employer or to a third party such as the leasing or disposal company as instructed by the employer.

Note that where the employee is provided with a motor car with zero CO2 emissions there is no taxable benefit in kind for 2020/21 although the charge increases to 1% of original list price for 2021/22.

Reimburse Private Fuel By 6th July To Avoid Fuel Benefit

Another consequence of the lockdown periods is that employees may have driven fewer private miles in their company cars, particularly where they have not been driving to the office.

If they are to avoid being taxed on the provision of private fuel they need to fully reimburse their employer for the cost of private fuel by 6 July 2021 for the 2020/21 tax year.

Note that the CO2 emissions percentage for the car is multiplied by the £24,500 notional list price used to calculate the benefit. For example, a director driving a Mercedes Benz E200 saloon company car (CO2 emissions 169g per km) would be assessed on 37% = £9065 for 2020/21. If they are a higher rate taxpayer then that means £3,626 tax. That would be an awful lot of private fuel!

In addition to the tax payable by the director on the provision of private fuel there would be £1251 Class 1A national insurance contributions payable by the employer.

Note that the private fuel benefit is an all or nothing benefit. There must be full reimbursement by 6 July to eliminate the benefit. The simplest method would be to multiply private miles by the HMRC advisory fuel rate for the vehicle.

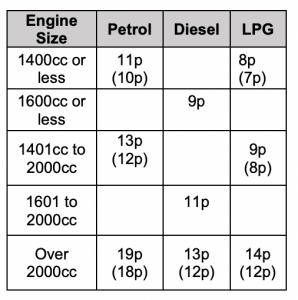

Advisory Fuel Rate For Company Cards

These are the suggested reimbursement rates for employees’ private mileage using their company car from 1 June 2021.

Where there has been a change the previous rate is shown in brackets.

Note that for hybrid cars you must use the petrol or diesel rate. You can continue to use the previous rates for up to 1 month from the date the new rates apply.

Please contact us if you would like to discuss any of the issues raised.